Methods

Our process, after determining which county we were going to analyze, was to collect the appropriate data for the variables determined in Project 2. We collected this data from the United States Census Bureau and standardized it so that each block group would be represented equally. Once we had performed these tasks we then, with the help of Dr. Lisa Keys-Mathews and Dr. Robertson, performed a factor analysis of our variables using SPSS software. After a process of trial and error, we eventually decided to run the process with ten components. The factor analysis essentially reduces redundancy in the data and combines related factors according to their relationship, whether that be positive or negative. As a result, we chose the three strongest components that we could recognize and created a series of cloropleth maps to label each block group according to its standing in each component. We tested some of our results using aerial imagery from Google Earth. For example, we compared areas of financial affluence and lack thereof on our maps with detailed imagery from Google Earth in order to determine the general accuracy of the factor analysis's groupings. Was financial affluence visible from the location, size, and environment of the housing?

The Factor Analysis

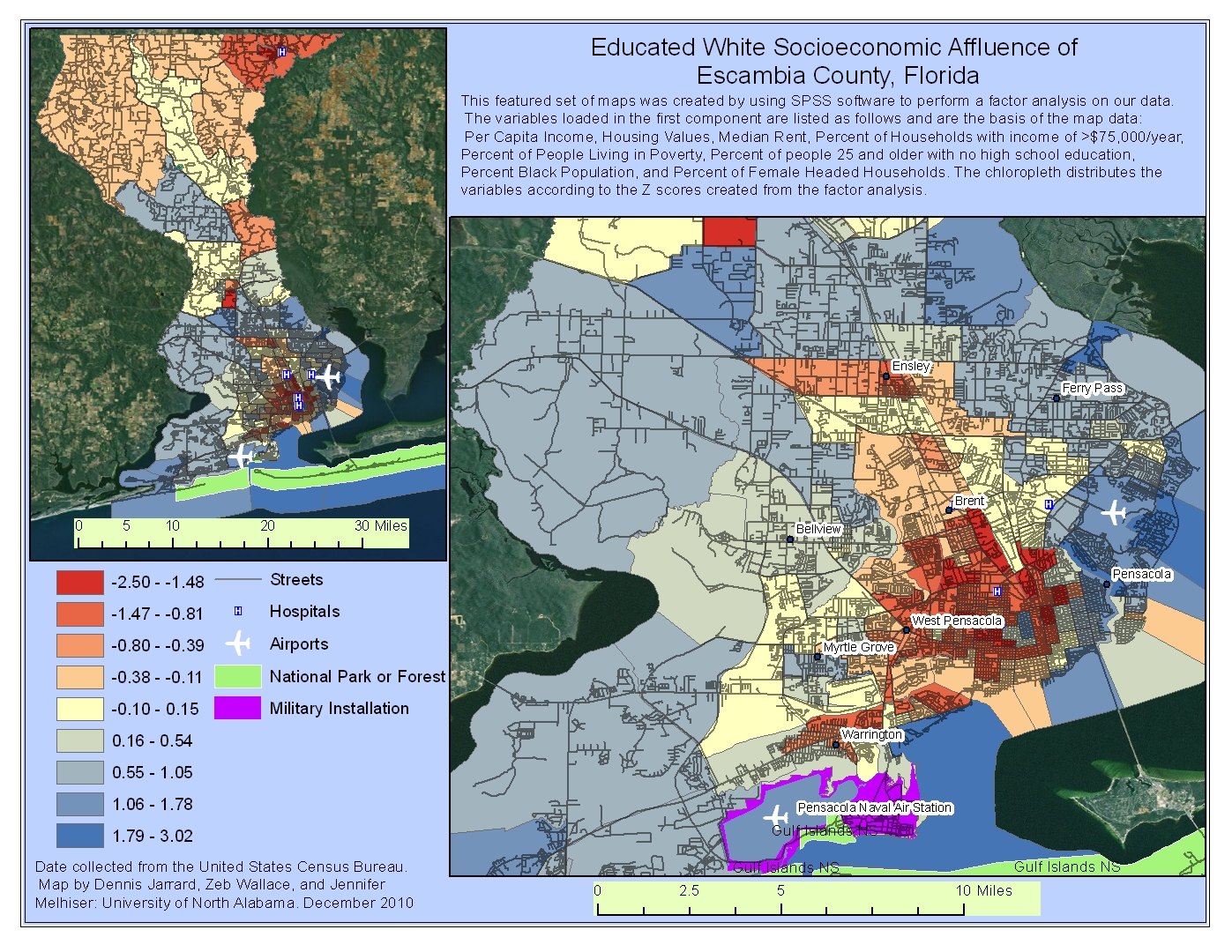

As previously mentioned, we selected the three strongest components in the factor analysis that we could recognize. We named the first factor "Educated White Socioeconomic Affluence" because of the variables that were loaded into the component. The following table represents the strongest variables that loaded and their relationship:

| Variable | Relationship |

|---|---|

| Per Capita Income | .882 |

| Housing Values | .824 |

| Median Rent | .772 |

| Percent of Households with income of >$75,000/year | .836 |

| Percent of People Living in Poverty | -.858 |

| Percent of people 25 and older with no high school education | -.863 |

| Percent Black Population | -.719 |

| Percent of Female Headed Households | -.741 |

To read the data, one only has to look at the numbers, as the positive values go up, the other positive values rise with it. However, as these values rise, the negative values decline and vise verce. For example, within the data in the previous table we can see that in Escambia County, as Per Capita Income goes up, Housing values go up, Median Rent goes up and the percentage of high-income families go up. However, as these factors rise, the percentage of people living under the poverty line go down (naturally), the percentage of adults living in the area with no high-school education goes down, the percentage of African Americans residing in the area goes down, and the percentage of female-headed households goes down. Therefore, we can then theorize that this particular component reveals white, educated, and affluent block groups within Escambia County.

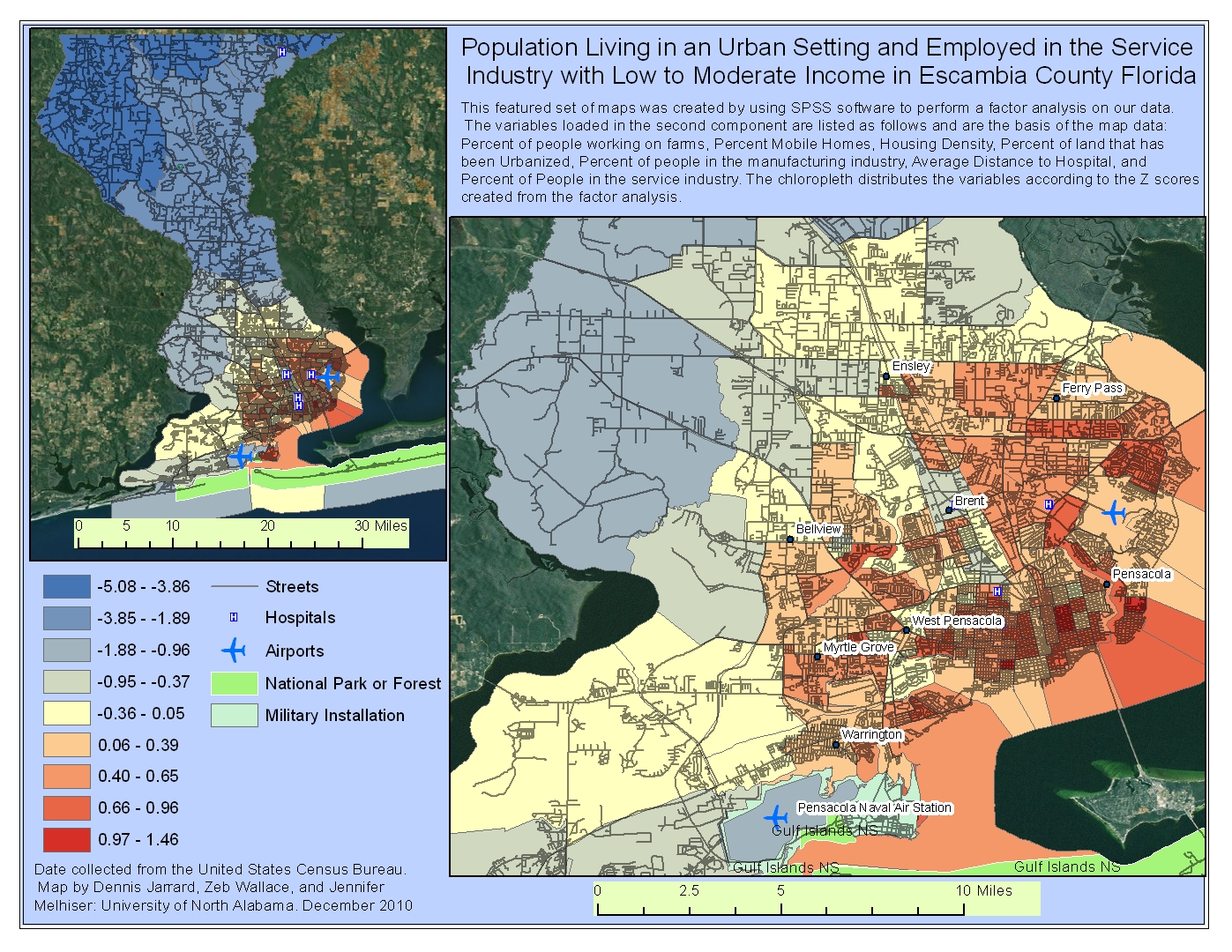

We then identified the second component as the Population Living in an Urban Setting and Employed in the Services Industry with Low to Moderate Income. Keep in mind that the higher the number ratings in the table, the stronger the relationship. We included a few lower loading variables, to show the general trend.

| Variable | Relationship |

|---|---|

| Percent of people working on farms | -.772 |

| Percent Mobile Homes | -.560 |

| Housing Density | .603 |

| Percent of land that has been Urbanized | .793 |

| Percent of people in the manufacturing industry | -.672 |

| Average Distance to Hospital | -.824 |

| Percent of People in the service industry | .595 |

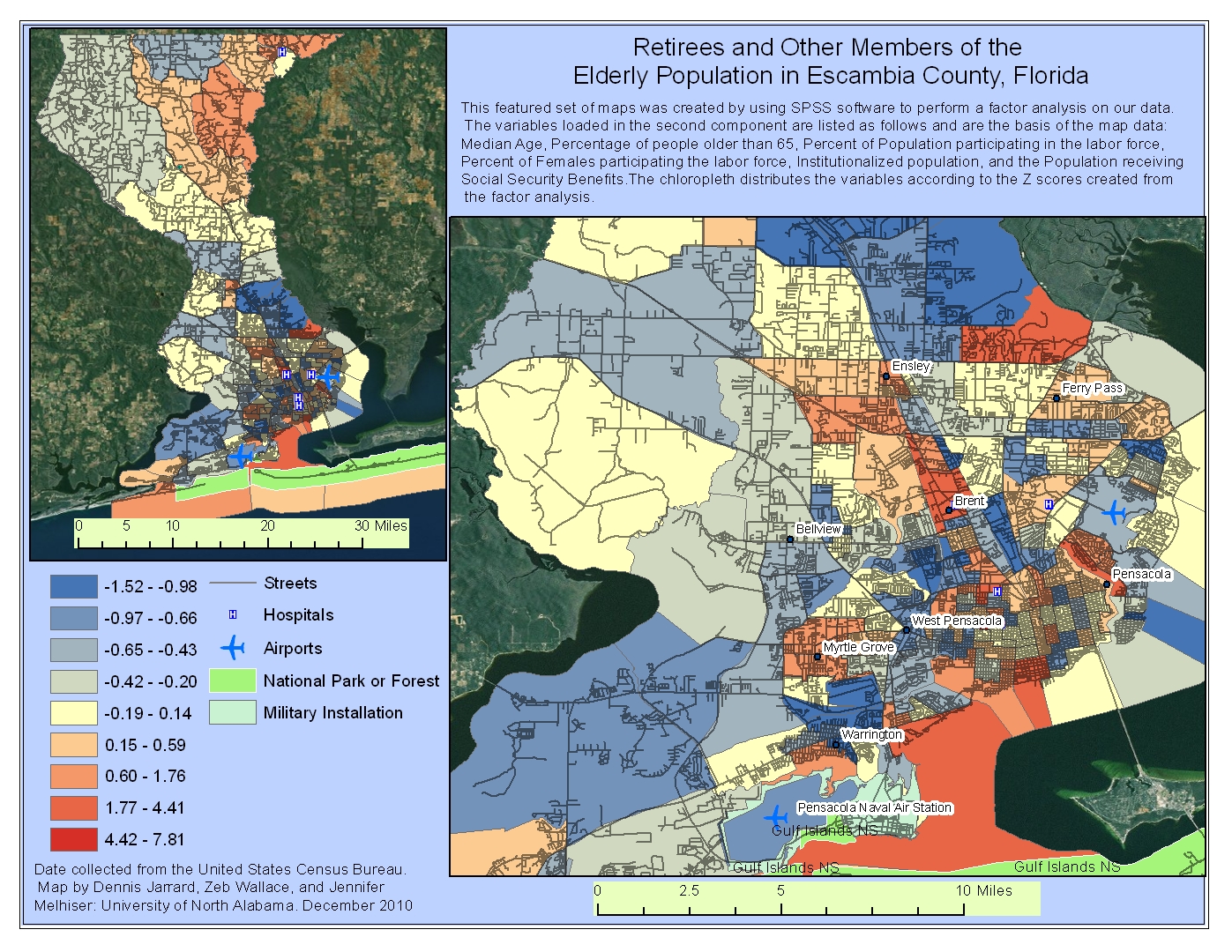

The third component that we selected seems to address retirees and other members of the elderly population.

| Variable | Relationship |

|---|---|

| Median Age | .675 |

| Percentage of people older than 65 | .856 |

| Percent of Population participating in the labor force | -.688 |

| Institutionalized population | .642 |

| Population receiving Social Security Benefits | .775 |

From this analysis we can conclude that in Escambia County the relationship between the number of people that are older than 65 and the number of people receiving social security benefits is very high, which is to be expected. There is also a positive relationship between these variables and a higher median age and percentage of people that are institutionalized (nursing homes, assisted living, etc.). These variables have a negative relationship with the percentage of the population participating in the labor force and the number of females participating in the labor force. Because of the components emphasis on the workforce, we tend to conclude that this component is addressing retired populations, but it does include other elderly populations as well.

Mapping the Components

After we had collected the data and performed the factor analysis, we then created three maps to demonstrate what our factor analysis revealed.

NOTE:Keep in mind that the each block group is color-coded according to its Z-Score. Imagine that 0 is the mean, and anything above 0 is above average and everything below zero is below average. For example, a z-score of 1.25 is equivalent to 1.25 standard deviations above the mean. Also, we used a color-scheme that portrays the more vulnerable side of the population as red. Not every map equates red with negative values as some variables actually reduce vulnerability.

On the first map (Map 1), the findings are rather logical. Much of the wealth in the area is concentrated around the coast while the dense inner city contains some the poorer areas.

Map 1: Click to Enlarge

Map 2 reveals some more information about the inner city and the levels of vulnerability present there.

Map 2: Click to Enlarge

Map 3 is meant to reveal some of the elderly, retired, and institutionalized populations.

Map 3: Click to Enlarge

Verifying the Analysis using Aerial Imagery:

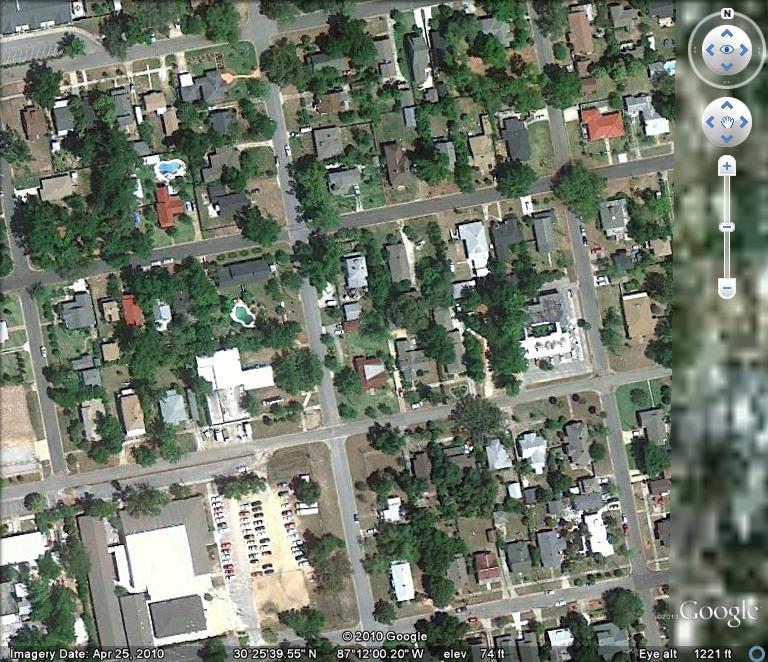

In order to test some of our assumptions, we decided to consult Google Earth imagery to analyze some of the areas that we theorized about. For example, did areas that appear wealthy on our chloropleth map have evidence in Google Earth imagery? Obviously, this is in no way an actual scientific process by which to establish theory. However, as this entire project was built from raw census data, we found it useful to make sure that our analysis was at least fairly accurate by aerial imagery standards. The first test was to determine if areas deemed "wealthy" by the index are visually wealthy. First, one of the wealthiest block groups portrayed on the map was selected.

Affluent Area

Impoverished Area

Densely Populated Area

Sparsely Populated Area